Assessing the impact of prevalence on pricing of rare disease drugs in Germany

In this first article of a three-part series exploring pricing in Europe, CRA’s Life Sciences Practice team discuss the role that disease rarity plays in reimbursement decisions among payers in Germany.

Historically, payers have accepted factors including small target patient populations and high clinical development costs as justifications for the high prices of rare disease drugs.

But as more companies develop and launch drugs to treat rare and ultra-rare diseases in Europe, the ability and willingness of payers to accept high prices may be reaching its limits. Payers must assess the budget challenges that new therapies might present against the goal of supporting access to innovative treatment options for as many patients as possible.

In these assessments, payers must often make determinations related to reimbursement based on data from a limited pool of eligible patients and potential gaps in efficacy and safety data, among other considerations.

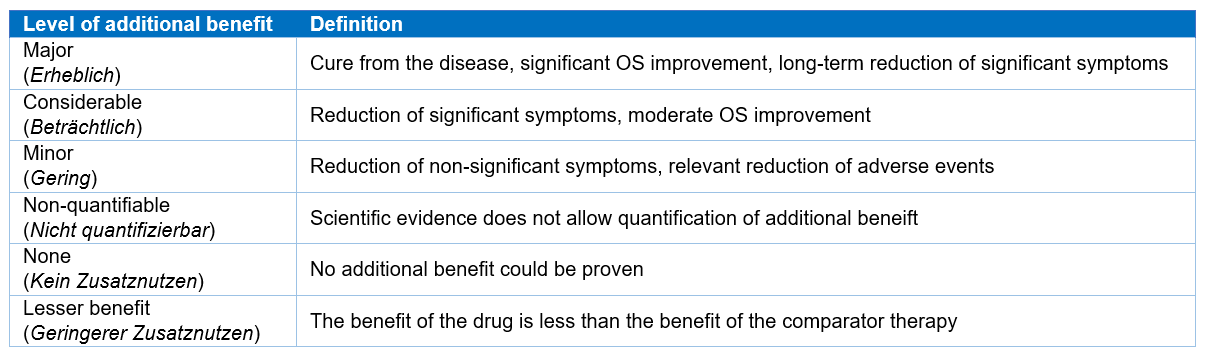

In 2011, government officials in Germany introduced legislation called the Arzneimittelmarkt-Neuordnungsgesetz (Act on the Reform of the Market for Medical Products, or AMNOG), which allows payers to assess products in accordance with evidence-based methods and weigh-up clinical benefit against budget impact. In this evaluation process, each product is given a rating representing the level of additional clinical benefit it provides – ranging from non-quantifiable or no benefit to considerable or major benefit.

For rare disease drugs, those with an orphan drug designation are guaranteed a positive additional benefit (at minimum, a non-quantifiable added benefit rating) if annual sales remain below €50 million. Any drugs that exceed this sales revenue are automatically re-assessed using the AMNOG process. Although this legislation has helped improve the assessment process, German payers still face uncertainties presented by rare diseases.

Overview of analysis: methods and goals

To better understand the range of factors payers focus on and the level of influence each has on reimbursement decisions for rare disease therapies, the team at CRA reviewed more than 20 rare and ultra-rare disease drugs that were recently approved in several European countries including Germany. We reviewed pricing for drugs including Kalydeco, Opsumit, Strensiq, and Galafold, assessing factors such as average annual treatment cost (AATC), disease prevalence rates, demonstrated added clinical benefit, and anticipated budget impact.

In our analysis, we used data from decision reports (Bechluss) from the G-BA (Gemeinsamer Bundesausschuss – Federal Joint Committee) and assessment reports produced by the IQWiG (Institut für Qualität und Wirtschaftlichkeit im Gesundheitswesen – Institute for Quality and Efficiency in Health Care). These reports were used to determine the number of patients eligible for treatment (prevalence) and to calculate the AATC based on the negotiated price. In cases where a rare disease drug has multiple indications, we focused on payers’ first assessment and first negotiated price to determine the AATC at that time.

The relationship between price and prevalence, among other factors

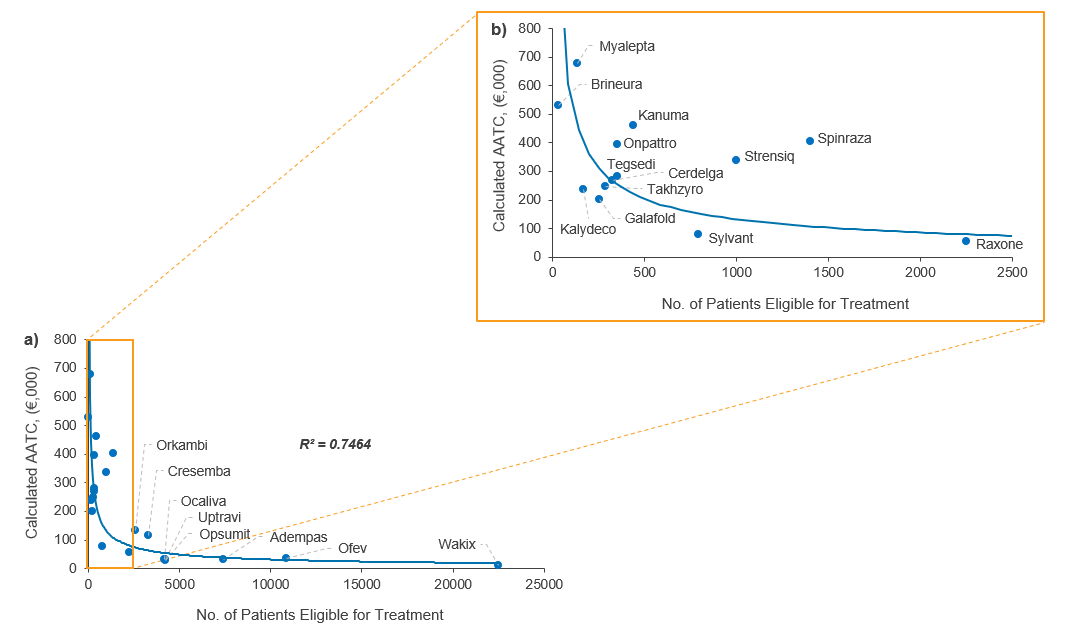

Across all European countries in this analysis, including Germany, we found a positive relationship between the list price of a rare disease drug and the rarity of the condition being treated – payers seemed willing to pay more for products expected to treat fewer patients. But this relationship was not straightforward in all cases. There were deviations from the trendline, as shown by Orkambi, Onpattro, Kanuma, Strensiq, and Spinraza, potentially because of other factors beyond prevalence that may influence payers’ willingness to pay, including:

- G-BA added benefit rating – this reflects several variables including robustness of safety and efficacy data and the level of additional clinical benefit associated with a rare disease drug compared to other available therapies. G-BA rating categories range from major added benefit – meaning potential curative benefit, improved overall survival, and long-term reduction of symptoms – to no added benefit proven.

- Clinical trial(s) comparator – documenting comparators that were used in the pivotal clinical trials as acknowledged in the G-BA decision; this ranges from active control to single-arm trials.

Table 1: G-BA added benefit rating and definition (Source: G-BA)2

Added benefit

More than half of the rare disease therapies (12 out of 22) reviewed in this analysis received an unquantifiable added benefit (AB) rating for their first indication, with the remainder receiving a mix of other ratings. There appears to be no overall correlation between AB rating and a more favourable price relative to disease prevalence.

But there are some cases where an AB rating may have had a significant impact on the list price. For example, the AATC of Orkambi, approved to treat cystic fibrosis patients with the F508del genetic mutation, may have been driven by the considerable AB rating. In turn, this may have increased payer willingness to reimburse Orkambi over other rare disease therapies with similar patient population sizes – such as Raxone for the treatment of Leber's hereditary optic neuropathy, which received an unquantifiable AB rating.

Like Orkambi, the RNAi therapy Onpattro also had a favourable AB rating that may have been a significant factor in the negotiated price. Onpattro achieved a considerable AB rating for the treatment of polyneuropathy caused by hereditary transthyretin (hATTR) amyloidosis, whereas its competitor Tegsedi received an unquantifiable AB rating. Despite being assessed at the same time with the same indication and eligible patient number, payers in Germany granted Onpattro a higher AATC compared to Tegsedi.

Spinraza is another example where the AB rating may have played a role in its achieved AATC. Among all the rare disease therapies reviewed in our analysis, Spinraza is the only one that received a major AB rating for the treatment of spinal muscular atrophy (SMA) type 1, along with a considerable AB rating for the type 2 sub-population. These favourable ratings may partly explain why it deviates from the positive relationship between price and rarity (as shown in Figure 1).

But AB rating is only part of the equation. For Uptravi, its benefit assessment resulted in an AB not proven rating in the treatment of adults with pulmonary arterial hypertension (PAH). But Uptravi achieved a similar AATC compared to other available treatment options for PAH including Opsumit, suggesting that in addition to AB rating, significant importance is attached to the size of the population and comparator pricing, to ensure similar costs for the same patient type.

Figure 1. Relationship between AATC and number of patients eligible for treatment in Germany (a) <25,000 patients eligible for treatment; (b) <2,500 patients eligible for treatment (Source: CRA analysis)

Clinical comparators

The use of drug comparators in clinical trials is another key factor that often drives G-BA decision-making and assessment of AB in Germany. These types of trials can range from single-arm trials with no comparator to active comparator trials where two comparable rare disease drugs are assessed based on data from multiple studies. But placebo-controlled trials are the most common protocol in the rare disease sector, and there is often no established standard of care to serve as a comparison.

Our findings indicate that clinical trial comparators do not significantly impact the ability to demonstrate an AB of rare disease therapies, demonstrating that payers are willing to value other factors including disease rarity, unmet need, and innovation in pricing negotiations. They likely consider clinical comparators in the context of a disease when determining an AB rating but more importantly focus on the robustness of the clinical data and the potential incremental benefit. For example, a number of rare disease drugs evaluated in placebo-controlled trials were able to achieve a minor or considerable AB rating in Germany, whereas all the drugs assessed in our analysis with active-control trials achieved unquantifiable AB ratings. Spinraza was the only rare disease therapy to achieve a major AB rating for patients with SMA type 1, following a trial comparing Spinraza versus best supportive care.

Conclusion

Payers in Germany assign some value to disease rarity, but it is only one of several factors in the equation during pricing negotiations. In addition, the relationship between price and prevalence does not appear to be linear, most likely due to other influential factors including the AB rating from the G-BA. While trial comparators are important, the quality of efficacy and safety data and certainty of the level of clinical benefit will often hold greater weight in payer assessments. While the AB rating may provide some initial negotiating power to manufacturers in rare disease, there also needs to be a solid understanding of the patient population size at the local level and how treatment uptake is expected to progress, both of which will likely impact payer willingness to pay for rare disease therapies. It is essential that manufacturers prepare early by conducting an audit of current treatment options (even including options for supportive care) and their associated costs, patient dynamics, and available clinical data to effectively negotiate an appropriate price for their orphan drug.

About the authors

Bhavesh Patel is a principal in the Life Sciences Practice at CRA and directs CRA's Rare Disease Issues Leadership Platform. He has experience in global pricing and market access, value proposition, commercial strategy, and launch readiness.

Cécile Matthews is a vice president in the Life Sciences Practice at CRA with 20 years of experience in strategy consulting for the pharmaceutical industry. Her areas of expertise include pricing, reimbursement, and market access globally.

Owen Male is an associate in the Life Sciences Practice at CRA. He has worked on numerous strategy and policy consulting projects focused on topics including pricing and market access, stakeholder engagement, commercial strategy, due diligence, and policy positioning.

The views expressed herein are the authors’ and not those of Charles River Associates (CRA) or any of the organisations with which the authors are affiliated.